")

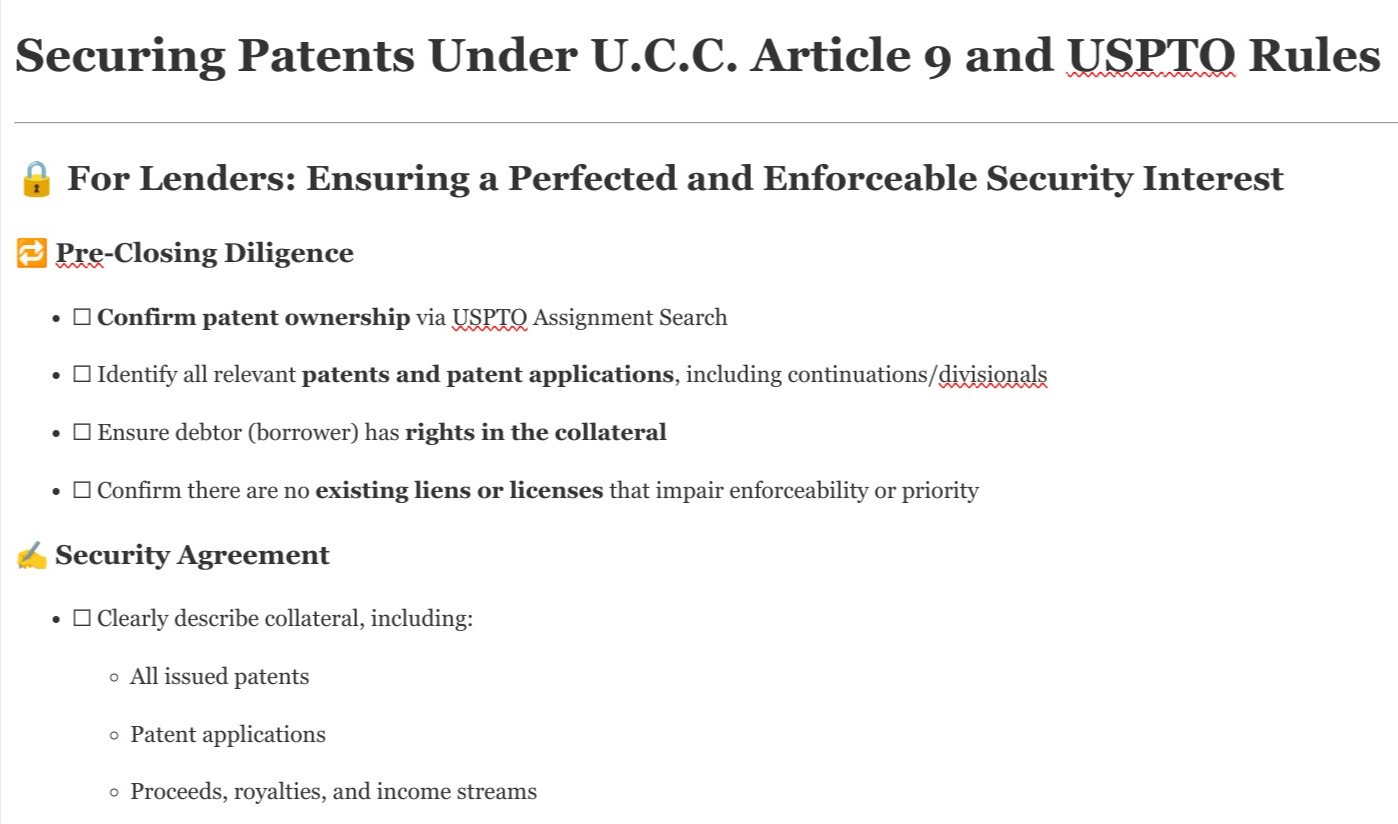

Before the loan, banks perform exhaustive due diligence to verify patent ownership, validity, and enforceability, ensuring compliance with OCC or Basel III guidelines that classify the loan as secured. During the term, they monitor patent status to avoid regulatory scrutiny or capital adequacy issues if the collateral deteriorates. Post-loan, banks need the patents to retain value for recovery in default, as any shortfall could trigger regulatory reporting obligations or impact their balance sheet health.

The Board of Directors hereby directs management to implement and maintain a Patent Portfolio Monitoring & Risk Disclosure System

When patent collateral weakens post-closing, lenders are often the last to know. A quiet shift in LTV can throw off your risk model—and cost you hundreds of thousands in annual return. Here's how it happens:

In an era of increasing shareholder activism and heightened board accountability, patent portfolio valuation and reporting isn't optional—it's an essential component of fiduciary duty for innovation-driven companies.

Systematic risk management isn't merely defensive—it creates competitive advantages through greater operational certainty and leverage in business negotiations.

Defective title chains are a silent killer of patent value. Real-world cases like Ethicon and Tri-Star underscore the financial and legal fallout of oversight.

Patent ownership disputes often arise when companies fail to explicitly secure rights to inventions created by employees or contractors.

The complexities and risks associated with encumbrances necessitate a proactive approach, underpinned by advanced technological solutions.

Patent enforceability hinges on effective maintenance fee management.